Bad Data

Jack Salmon, Research Fellow at the Mercatus Center and author of the Substack The Unseen and The Unsaid (and recent podcast guest!) has a great piece out this week that tears down the myth popular among tax hike advocates these days.

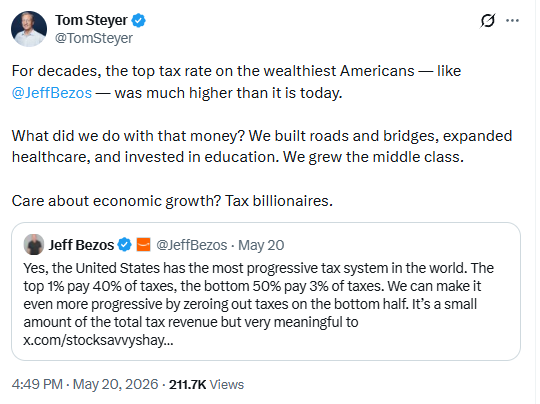

The writeup was inspired by a post on X from Tom Steyer, billionaire and California gubernatorial candidate, making a familiar argument: top tax rates were sky-high in the postwar decades, and all that revenue built the middle class.

This claim surfaces reliably in every tax debate, deployed to suggest that …

(Read More)